Global Manufacturing Outlook: Opportunities and Challenges for Machine Tools in 2026 (Part I)

Global and Taiwan Machine Tool Output Expected to Grow in 2026

In 2025, global manufacturing showed a pattern of “moderate growth with structural divergence.” Major economies faced persistent inflation, rising trade protectionism, and geopolitical risks. According to IMF and OECD forecasts, global economic growth will remain around 3%, providing a foundation fora mild recovery in manufacturing. Growth will be driven primarily by high-value industries such as AI, semiconductors, and aerospace, while automotive and general machinery demand will grow slowly due to high costs and conservative purchasing by end-users.

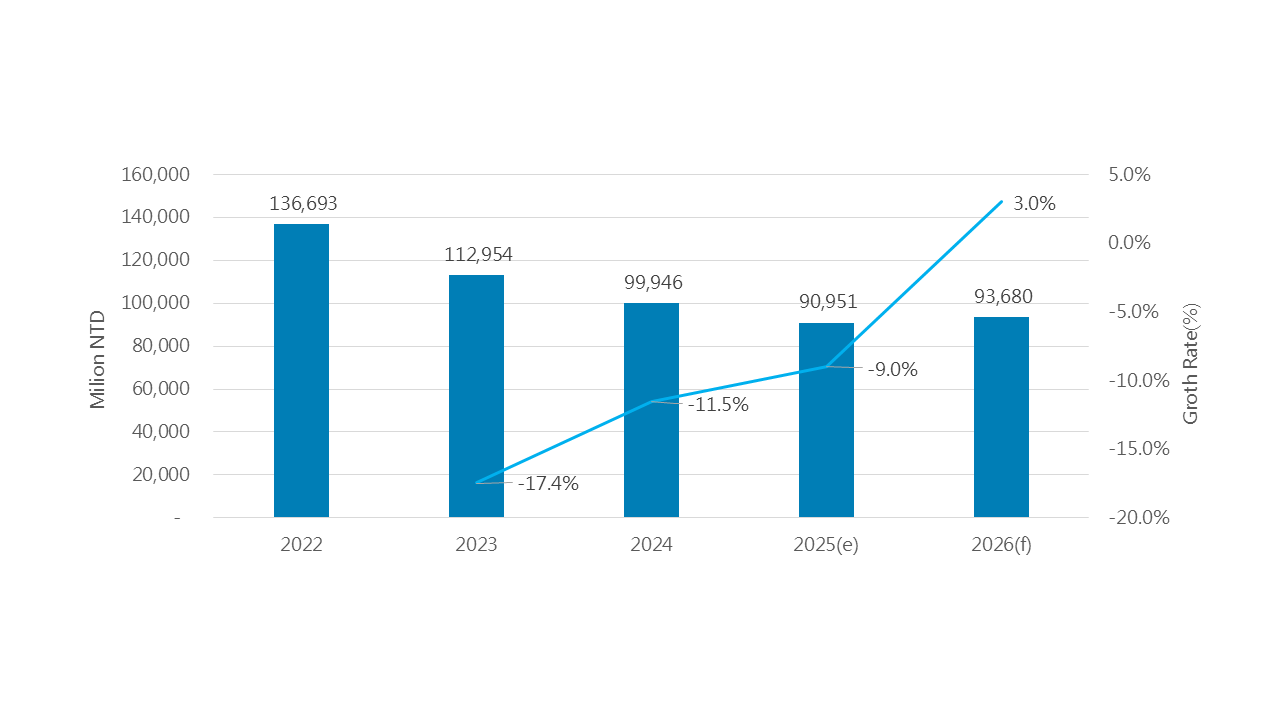

The global machine tool industry is expected to gradually recover from the downturn in 2024, with growth concentrated in high-end applications such as aerospace titanium-aluminum alloy machining, semiconductor/precision components, and upgrades to smart machines. Investments in “smart manufacturing”—integrating automation, sensors, edge computing, and AI predictive maintenance—are becoming a common trend in industrial upgrades worldwide, benefiting core component suppliers such as those producing controllers, linear guides, ball screws, and spindles.

Demand varies significantly by region: China remains sluggish; the U.S. faces inflation and weak domestic demand; Europe struggles with high energy costs; India and Southeast Asia, by contrast, maintain steady expansion, emerging as bright spots for global machine tool exports.

Taiwan’s manufacturing sector continues to grow, driven by AI servers, semiconductor expansion, and electronic component demand. However, the machine tool industry’s rebound is limited due to declining demand from China, tariff uncertainties in the U.S., pricing pressure from a weak yen, and slow European markets. Companies with capabilities in semiconductor/PCB equipment components, high-speed and high-precision machining, or smart integrated production lines are expected to outperform the market.

Looking ahead to 2026, the global machine tool market is expected to sustain the recovery pace of 2025, characterized by “moderate growth with structural divergence.” Key drivers include aerospace component machining, precision parts demand, and accelerated adoption of automation and smart equipment worldwide. Growth will focus on five-axis machining centers, high-speed/high-precision models, hybrid/3D printing processes, and smart machines equipped with sensors and AI. Geopolitical tensions and supply chain restructuring remain critical variables; tight monetary and tariff policies could suppress investment in mid- and low-end capital equipment, while expansion in emerging manufacturing hubs such as India and Southeast Asia will support exports.

For Taiwan, 2026 will continue the trend of “overall manufacturing growth with machine tool divergence.” AI and semiconductors will boost the electronics supply chain, benefiting companies with high-precision machining or semiconductor component capabilities. Traditional exporters focusing on mid- and low-end models will face threefold pressures from exchange rates, price competition, and conservative investment, with order recovery likely lagging behind the global average. The key to achieving a breakthrough lies in transformation: entering AI/semiconductor equipment and aerospace/defense supply chains, deepening customization for specialized machines, promoting smart machines and integrated solutions, and strengthening presence in emerging markets. Overall, 2026 will see “gradual global growth” for machine tools, while Taiwan will experience a “stable high-end segment and pressured mid- to low-end segment.”

|

Geopolitics, Energy Prices, Inflation, and Interest Rates: Key Factors Shaping the Industry

The future of the machine tool industry will be driven by multiple factors, including geopolitics and trade policies, energy and raw material prices, inflation and interest rates, end-market demand shifts, and digital transformation technologies such as AI and digital twins. These factors collectively influence global supply chain layouts and capital spending decisions.

Geopolitical tensions and tariffs will reshape supply chains and procurement strategies, pushing customers toward politically aligned or stable regions. Globally, this will accelerate regionalized production and the rise of local suppliers. For Taiwan, this presents both opportunities (regional outsourcing and order transfers) and risks (export restrictions or additional U.S. tariffs).

Energy and raw material costs, along with inflation and interest rates, determine the pace of capital spending. Rising costs and higher interest rates will delay equipment purchases, making mid- and low-end machine demand more vulnerable. Only high-value, automated, and energy-efficient machines remain attractive. Technological advances continue to create demand for high-end machines—those featuring AI predictive maintenance, digital twins, hybrid/3D printing, or five-axis capabilities—which will become the preferred choice for manufacturing upgrades worldwide, and a key direction for Taiwanese manufacturers.

Other influencing factors include core component supply, which affects lead times and quality. Companies controlling critical parts will gain bargaining power and growth opportunities. Exchange rate fluctuations and monetary policies directly impact price competitiveness; a weaker yen or euro squeezes Taiwan’s export margins. Environmental regulations and corporate carbon reduction goals drive low-energy machining and circular manufacturing, prompting equipment upgrades. Finally, regional market expansion (India, Southeast Asia, Central and Eastern Europe, Latin America) offers alternative export opportunities and growth platforms, requiring localized operations and service networks.

The global machine tool market is moving toward a structure characterized by “growth in high-end and smart solutions, pressure on low-end volume and pricing.” For Taiwan, leveraging precision manufacturing strengths, enhancing in-house production of key components, accelerating smart and service-oriented transformation (MaaS/data services), and expanding into India and Southeast Asia will turn external risks into competitive advantages. Conversely, continued reliance on traditional mid- and low-end exports without digital upgrades will leave Taiwan disadvantaged in global restructuring.