CommonWealth Magazine Top 2000 Enterprises Survey: Taiwan’s Machine Tool Industry Demonstrates Strong Resilience and a Divergent Industry Landscape in 2025

Known as the “mother of machinery,” machine tools are not only an important indicator of a nation’s manufacturing strength and level of industrial modernization, but also a cornerstone supporting the development of high-end manufacturing sectors such as aerospace, automotive, and semiconductors. Looking back at recent developments, Taiwan’s machine tool industry rebounded from the prolonged downturn caused by the COVID-19 pandemic in 2022, as demand from application sectors recovered and equipment investment gradually picked up.

However, entering 2023, the global manufacturing climate did not improve as smoothly as expected. Although industrial production and end-market demand were expected to recover as the impact of the pandemic gradually faded, global geopolitical conflicts intensified, including the Russia-Ukraine war, tensions in the Middle East, and the U.S.-Iran conflict. These developments pushed up energy prices and inflationary pressures. In April 2025, the United States announced “reciprocal tariffs” on 185 countries and regions, further intensifying global trade frictions. Under the combined impact of volatile exchange rates, high tariffs, and the deepening U.S.-China trade war, global supply chains underwent drastic restructuring, leading companies to adopt more conservative capital expenditure strategies and significantly suppressing global manufacturing investment demand.

Taiwan’s machine tool and components industry demonstrated remarkable industrial resilience

In 2025, Taiwan’s total machine tool exports declined to US$2.004 billion, down 9.6% from 2024. Machining centers remained the largest export category, with exports of approximately US$603 million, accounting for about 30% of total machine tool exports and representing an 8.33% year-on-year decline. Lathes ranked second, with exports of approximately US$430 million, accounting for about 22% of total exports and falling 18.3% year on year. In contrast, grinding machines achieved slight growth of 2.4% amid adversity, indicating that global demand for high-end precision equipment remained strong.

On the import side, Taiwan’s machine tool market showed strong momentum driven by semiconductors and high-end manufacturing transformation. In 2025, total machine tool imports reached US$643 million, up 16.4% from 2024. Electrical discharge and laser processing machines ranked first among metal-cutting machine tool imports, with import value of approximately US$253 million, accounting for 39% of total imports and growing 8% year on year. Machining centers ranked second, with import value of approximately US$120 million, accounting for 19% of total imports and increasing 66.4% year on year. Forging and stamping machines as well as other forming equipment also posted explosive growth of nearly 60% and 1.6 times, respectively.

This indicates that the structure of domestic and overseas markets is gradually changing. While overseas general-purpose markets have been weakened by geopolitical risks and tariffs, domestic demand in Taiwan for high-precision, non-traditional processing, and automation-integrated equipment has risen significantly. This highlights the urgency for Taiwan’s machine tool products to transition from mid- to low-end conventional complete machines toward high-value-added intelligent equipment. If companies continue to rely on the traditional one-time hardware sales model, it will be difficult to respond to current changes. Instead, they must deepen their presence in niche markets, strengthen cooperation with high-value application supply chains such as semiconductors, aerospace, and medical devices, and transform from single-machine exports into integrated solutions centered on AI and intelligence. Only by enhancing product value-added can the industry break through amid the restructuring of global manufacturing.

Taiwan Machine Tool Industry at a Crossroads: High-End Accessories Rise as Machine Makers Seek New Openings

According to CommonWealth Magazine’s 2026 Top 2000 Enterprises Survey, based on 2025 data, the overall manufacturing environment remained challenging. In the machine tool and components industry, complete machine manufacturers were generally under pressure due to conservative capital expenditures and rising energy and transportation costs, while component suppliers showed stronger resilience by entering demand-driven sectors such as semiconductors, aerospace, and new energy.

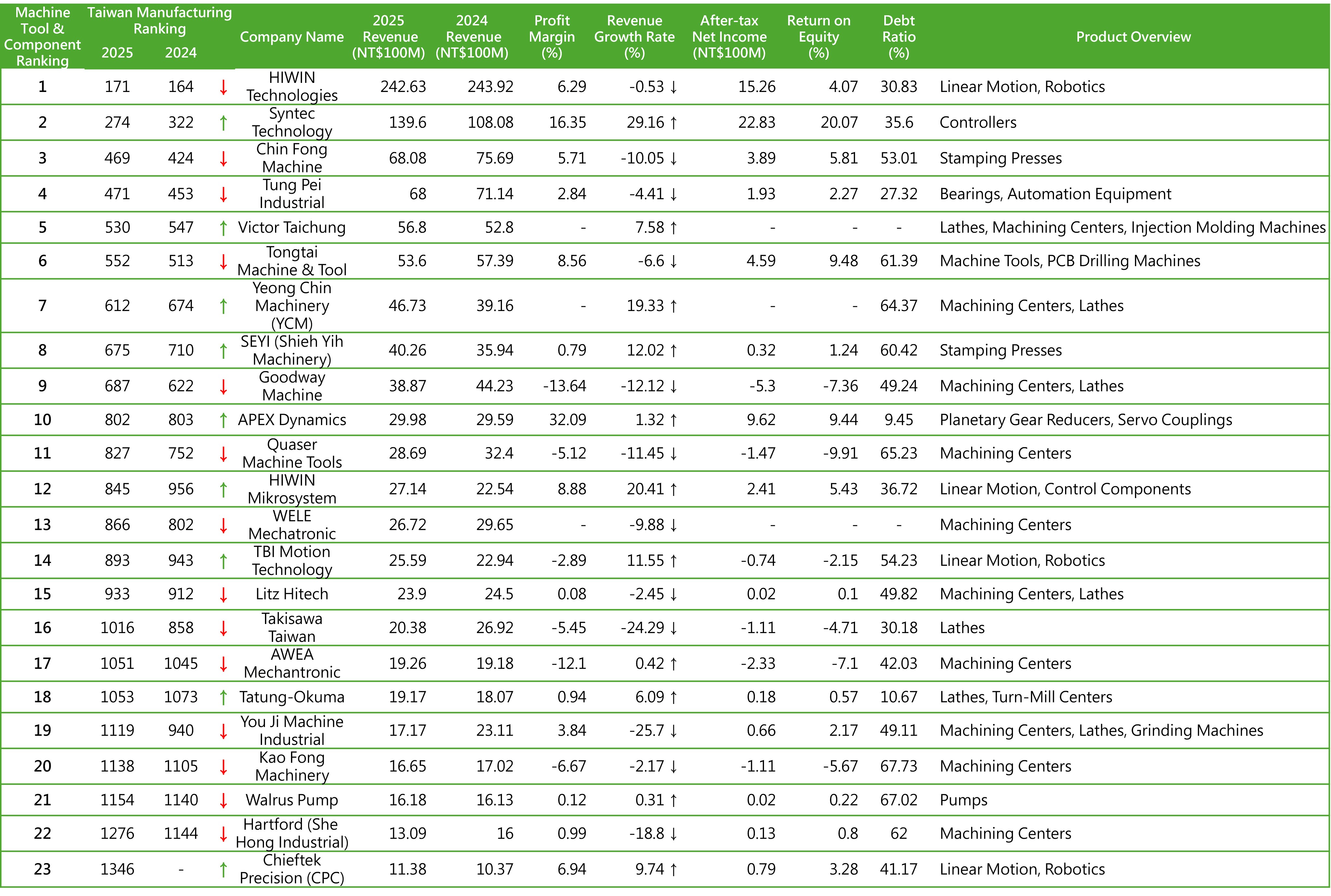

In the 2025 Top 2000 Enterprises Survey, a total of 23 companies from the machine tool and components sector were listed. By ranking, the overall industry showed signs of divergence: some high-end component suppliers advanced in ranking, while most complete machine manufacturers declined. In terms of revenue, leading companies maintained scale advantages. Among the listed companies, 48%, or 11 companies, recorded revenue growth, while 52%, or 12 companies, faced pressure from the broader environment. The industry’s resilience therefore showed a clear polarization.

Among machine tool component companies, HIWIN Technologies, a leading transmission component manufacturer, reported consolidated revenue of approximately NT$24.263 billion in 2025, down 0.53% year on year. Nevertheless, its core technologies in linear transmission and robotics continued to secure its global market position. With booming demand for AI robotics and advanced semiconductor packaging, such as panel-level packaging and silicon photonics, HIWIN not only showcased intelligent solutions with Qualcomm at COMPUTEX this year, but also emphasized in its investor conference that it would actively transform from a component supplier into a provider of high-end automation solutions. The share of robotics revenue in the first quarter doubled from the previous 5% to 7% range to 12%.

At the same time, demand from semiconductor and robotics applications spilled over into Taiwan’s core component supply chain. HIWIN Mikrosystem posted counter-cyclical revenue growth of approximately 20.41%, reflecting strong demand from semiconductor processes for high-value-added nano-level positioning platforms. TBI Motion also recorded year-on-year growth of 11.55%. The company further adjusted its capacity allocation this year: its Suzhou plant will focus on high-volume standardized products, while its Taiwan plant will gradually shift toward high-end applications such as robotics, automotive, semiconductors, and medical industries.

Meanwhile, Syntec Technology, a hidden champion in controllers, also delivered impressive results. In 2025, its revenue reached NT$13.96 billion, up nearly 30%. In addition to successfully capturing order transfers from Japanese major FANUC through an early inventory strategy, Syntec has partnered with its subsidiary Leantec Intelligence to target AI server liquid cooling, new energy vehicles, and robotics applications. The company has set a goal of deploying 10,000 CNC loading and unloading robots within three years.

AI, Automation, and Niche Markets: Three Pathways for Machine Makers’ Transformation

In the revenue ranking of complete machine manufacturers, most companies saw revenue decline by 10% to 20%, although domestic manufacturers continued to demonstrate industrial resilience. Goodway Machine’s revenue fell 12.12%, but in 2026 the company formed an alliance with controller leader Syntec Technology to develop AI intelligent control and automation solutions to enhance product competitiveness. Taiwan Takisawa’s revenue declined 24.29%. At the 2026 TMTS exhibition, the company stated that it would expand into emerging markets such as AI server water-cooling systems, drones, and high-precision electronic components, gradually transforming from single-machine sales into a total solution provider. Researching machining speed and quality for niche industries has become a key direction for industrial development which supported orders for high-end models such as high-precision spindles and large vertical machining equipment.

Overall, Taiwan’s complete machine tool market is accelerating the application of smart manufacturing and robotics technologies through independent research and development as well as cross-sector collaboration. These efforts aim to increase product value-added, strengthen global service capabilities, and drive the industry’s transformation toward a smart manufacturing ecosystem.

In summary, under the pressure of market structural divergence, Taiwan’s machine tool industry is at a critical stage of product upgrading and business model transformation. If companies can leverage their existing strengths in precision manufacturing and a complete supply chain while actively aligning with trends toward intelligence, green transformation, and high-end development, they will be better positioned to capture substantive opportunities in high-end components and smart manufacturing, thereby building an internationally competitive and sustainable industrial structure.

|

Source: CommonWealth Magazine 2026 Top 2000 Enterprises Survey Ranking Database; compiled by PMC.