2026 Trade Policy Barometer: What Are the Next Moves of Major Economies and How Will They Reshape Taiwan’s Machine Tool Industry?

Global and Major Economies’ Growth Outlook for 2026

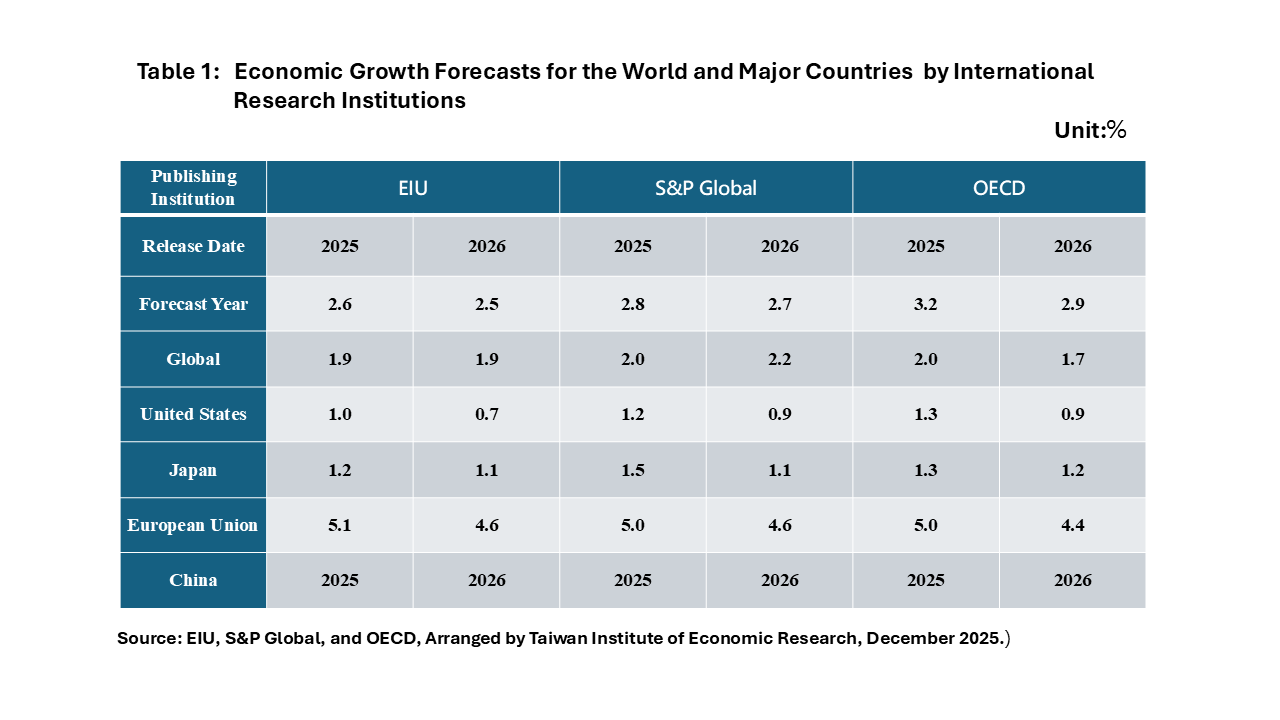

According to forecasts from multiple international research institutions (see Table 1), global and major economies are expected to maintain steady growth in 2026. Signs of easing tensions emerged from the fifth round of trade negotiations between the United States and China in Malaysia, while supply chain relocation continues to drive economic expansion in ASEAN countries. These factors are likely to boost global manufacturing investment confidence and, consequently, increase demand for machine tools. However, uncertainties such as the Russia-Ukraine war, Middle East conflicts, geopolitical tensions between India and Pakistan, Thailand and Cambodia, deteriorating China-Japan relations, and potential renewed trade sanctions between China and the United States may still affect global economic performance in 2026. The following sections analyze major economic and trade policies in key countries closely linked to Taiwan’s machine tool industry, either as important markets or major competitors.

United States

In April 2025, President Trump introduced a reciprocal tariff policy, prompting international corporations and domestic firms to expand investments in the U.S. The government also promoted onshoring of critical manufacturing sectors, focusing on AI, advanced technologies, and high-value-added industries through tax incentives and investment subsidies. This remains a key fiscal policy direction for 2026.

On monetary policy, the Federal Reserve announced in December 2025 its plan to purchase $40 billion in U.S. Treasury securities monthly during 2026 to maintain financial stability and prevent liquidity shortages—distinct from traditional quantitative easing. Meanwhile, reciprocal tariffs have triggered imported inflation, suggesting that interest rate cuts will continue in 2026, albeit modestly.

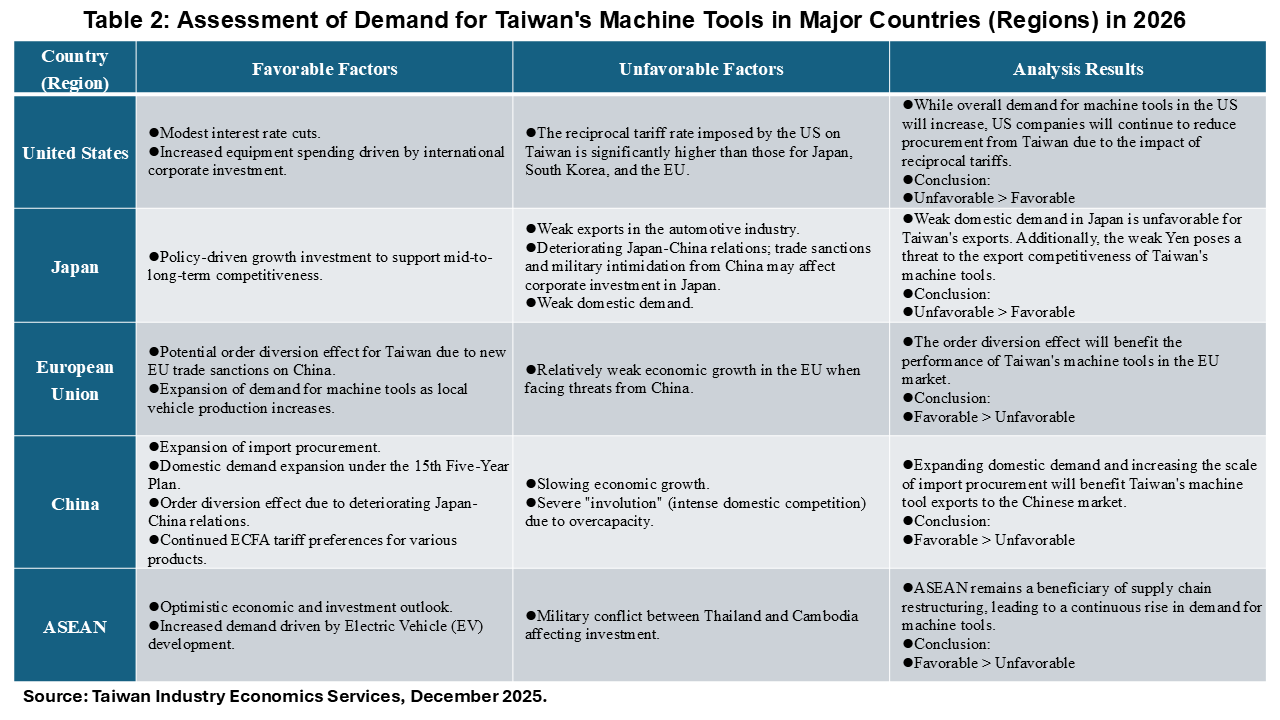

In the automotive sector, the cancellation of EV purchase subsidies will dampen electric vehicle sales, prompting automakers to pivot toward hybrid vehicles, which may increase demand for machine tools. However, the U.S. reciprocal tariff rate on Taiwanese products (20%+N) is significantly higher than that applied to Japan, Korea, and the EU, severely impacting Taiwan’s machine tool exports to the U.S.

Japan

On December 19, 2025, Japan raised interest rates by 25 basis points to 0.75%, signaling the end of nearly three decades of ultra-loose monetary policy. While moderate rate hikes are likely in 2026, they may improve capital allocation efficiency and corporate profitability. Japan’s industrial policy emphasizes AI, semiconductors, advanced manufacturing, and shipbuilding across 17 priority investment areas. However, direct support for machine tools remains limited. Additionally, U.S. Section 232 tariffs imposed a 25% surcharge on Japanese automobiles, later reduced to 15%—still significantly higher than the previous 2.5%, weakening Japan’s auto exports and reducing machine tool demand. Yen depreciation has made Japanese high-end machine tools more price-competitive, posing a threat to Taiwan’s exports.

European Union

In 2026, the EU faces challenges from U.S. trade policies, Chinese competition, and geopolitical risks, striving to balance “de-risking” with growth. Widening trade deficits with China may prompt new sanctions, potentially benefiting Taiwanese firms through order transfers. Furthermore, the EU relaxed its 2035 ban on internal combustion vehicles, instead requiring a 90% reduction in average carbon emissions from 2021 levels, aiming to curb Chinese EV dominance and boost local auto production—likely increasing machine tool demand.

China

2026 marks the first year of China’s 15th Five-Year Plan, emphasizing “high-quality development” through technological self-reliance, domestic demand expansion, and enhanced national security. Policies supporting next-generation IT and high-end manufacturing will strengthen China’s machine tool industry, intensifying competition for Taiwan. Additionally, strained cross-strait relations led to the suspension of tariff concessions on four machine tool products under ECFA, raising import duties to 5–9.7%, which significantly reduced Taiwan’s exports to China in 2024–2025. While relations remain tense, China’s record trade surplus in 2025 may drive increased imports to avoid sanctions, benefiting Taiwanese exporters still enjoying ECFA tariff reductions.

ASEAN

Despite recent military tensions between Thailand and Cambodia, ASEAN’s economic outlook remains positive for 2026, supported by accommodative monetary conditions, robust domestic demand, and spillover effects from technology industries. Vietnam’s rapid rise as a regional growth engine and strong EV development in Thailand and Vietnam will sustain machine tool demand.

Conclusion

Global monetary conditions are expected to remain accommodative in 2026, and investment enthusiasm in AI and advanced technologies will persist, supporting machine tool demand. However, tariff wars and geopolitical risks will create divergent outcomes across markets: U.S. and Japan orders may decline, while demand from the EU and ASEAN will rise. China’s shift toward expanded imports could also revive Taiwanese exports if firms actively pursue opportunities (see Table 2 for detailed market assessments).