Stop, Look, Listen: The Corporate Sustainability Due Diligence Directive Will Reshape Europe’s Supply Chain Network

By Ou Yi-Pei, Senior Researcher, ITRI ISTI

Due to the impact of COVID-19 and geopolitical factors, global supply chains have undergone significant changes, requiring companies to strengthen risk management to align with sustainability goals. The implementation of the EU Corporate Sustainability Due Diligence Directive (CSDDD) marks a major milestone. It will mandate large companies to conduct due diligence across their global supply chains to identify, prevent, and mitigate environmental and human rights risks and impacts. Only by prioritizing supply chain transparency and comprehensive risk management can businesses maintain competitiveness and sustainability in a volatile environment.

1. CSDDD as a Milestone: Mandatory Due Diligence for Companies

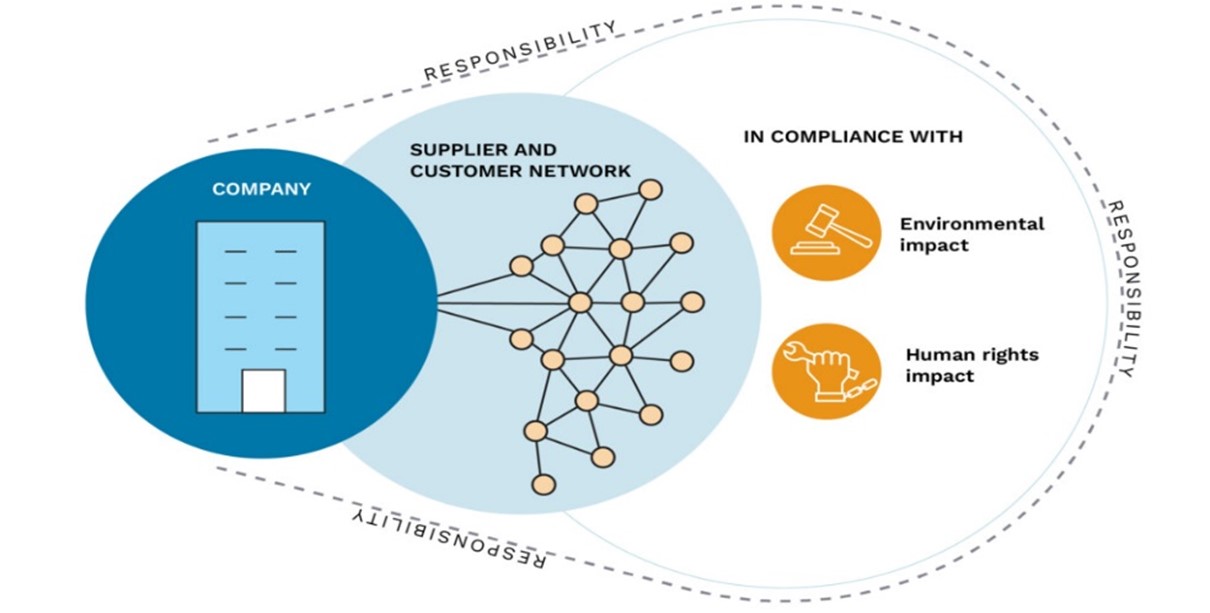

Global supply chains involve multi-tier supplier networks, making it difficult for a single company to have full visibility. For example, the EU plans to replace fuel-powered cars with electric vehicles, which require critical minerals like cobalt often mined in African countries such as the Democratic Republic of Congo. These minerals pass through multiple layers of transactions before reaching European EV manufacturers. However, these mines often fail to meet EU environmental and human rights standards. Without transparent traceability, European EV companies risk violating EU sustainability standards.

Such cases are not rare but often hidden within supply chains or overlooked for cost reasons. To address this, the EU proposed CSDDD in 2021. After several hurdles, the European Parliament approved it on April 24, 2024, published it in the Official Journal on July 5, and it took effect on July 25. Large companies will be required to implement human rights and environmental due diligence in their supply chains starting as early as 2027.

|

Source: Everstream Analytics (2024)

|

Source: Compiled by ISTI of ITRI (2024)

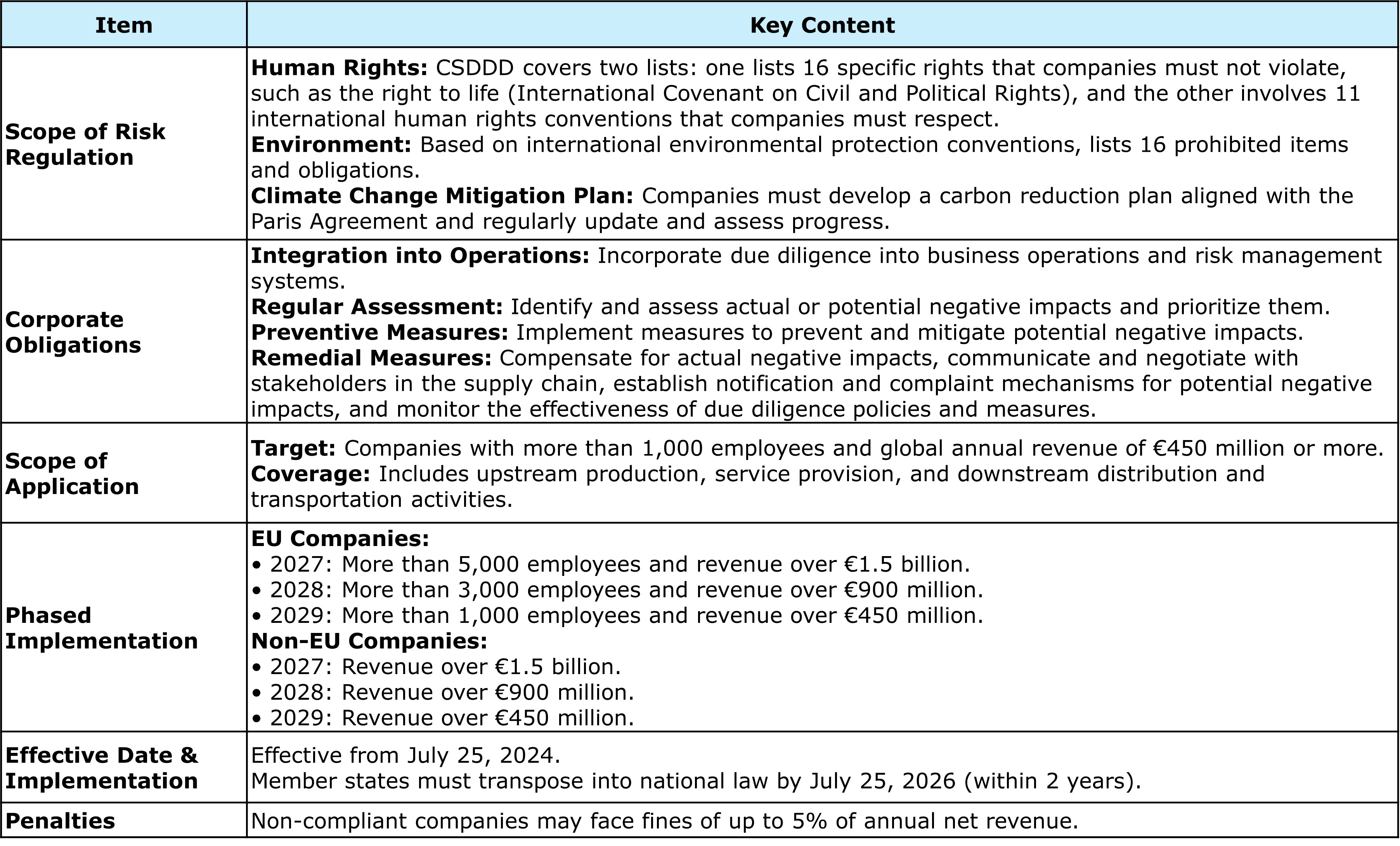

Key Highlights

- Scope of Risks: Human rights and environmental risks, with emphasis on climate transition planning.

- Corporate Obligations: Integrate due diligence into operations and risk management systems, regularly assess potential negative impacts, implement preventive and remedial measures, and establish grievance mechanisms.

- Applicability: Companies with over 1,000 employees and global revenue exceeding €450 million, including non-EU firms operating in the EU.

- Phased Implementation:

- 2027: >5,000 employees and €1.5 billion revenue

- 2028: >3,000 employees and €900 million revenue

- 2029: >1,000 employees and €450 million revenue

- Penalties: Up to 5% of global net turnover for non-compliance.

- Reporting: From July 2029, companies must publish annual due diligence statements and submit reports to the EU’s European Single Access Point (ESAP) platform.

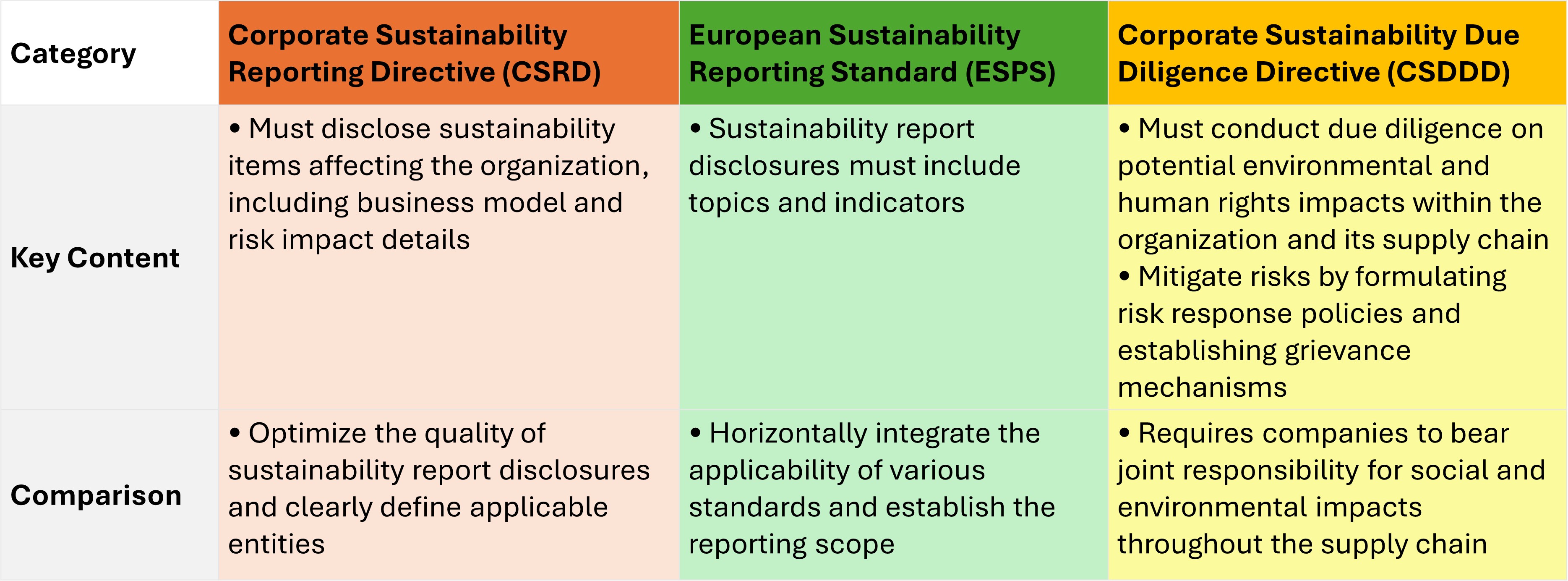

2. Comparison with Other EU Sustainability Regulations

- CSRD (Corporate Sustainability Reporting Directive): Expands non-financial reporting to include ESG standards.

- ESPS (European Sustainability Reporting Standard): Specifies detailed reporting requirements under CSRD.

- CSDDD: Focuses on supply chain human rights and environmental risks, imposing mandatory due diligence and shared responsibility.

|

Source: Compiled by ISTI of ITRI (2024)

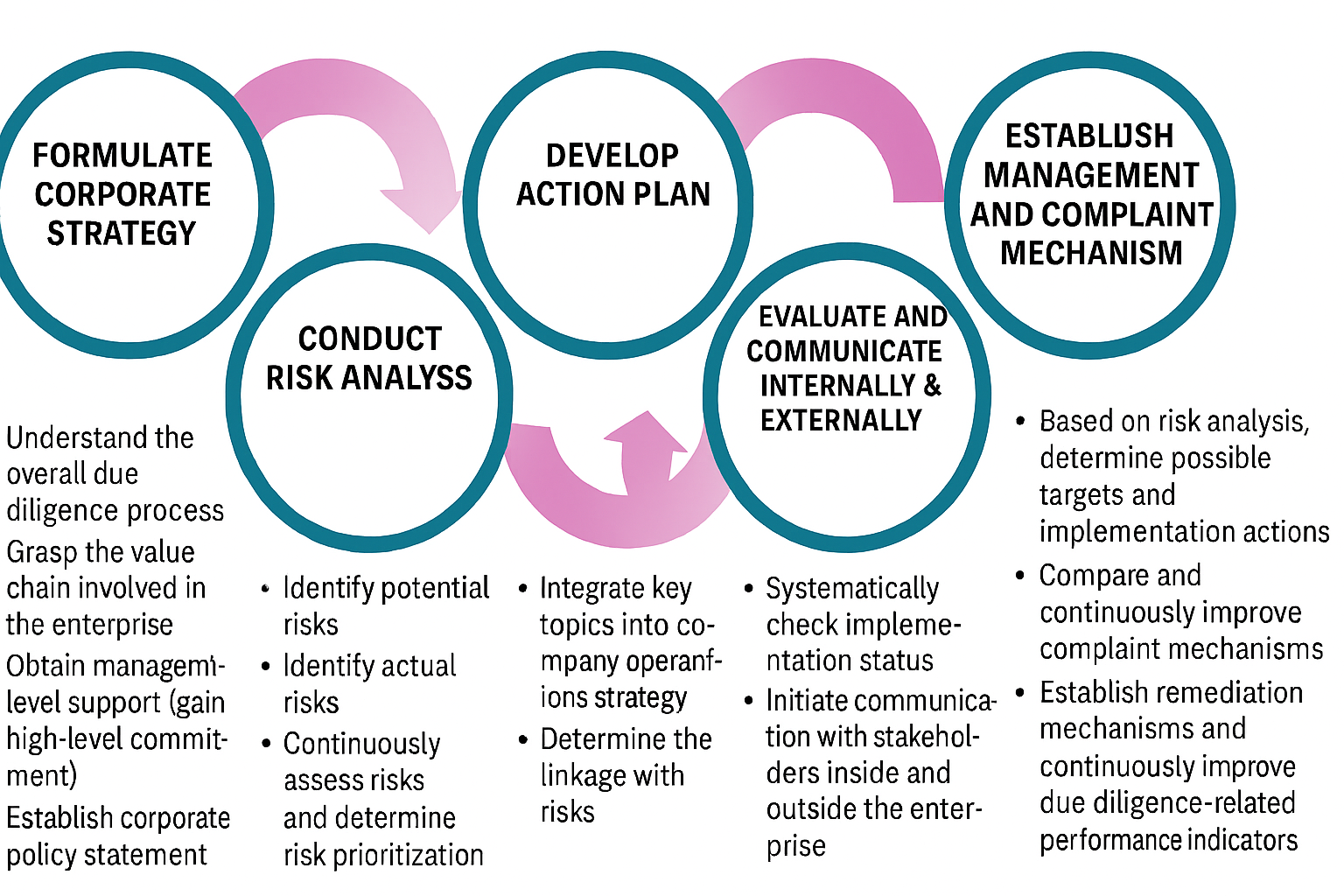

3. Lessons from Germany’s Supply Chain Due Diligence Act

- Companies may shift sourcing to avoid compliance risks.

- SMEs, though not directly regulated, may face indirect pressure from larger firms.

- Challenges include supplier data transparency, cross-cultural collaboration, continuous monitoring, and implementing new digital tools.

|

Source: European Parliament (2024),Compiled by ISTI of ITRI (2024)

4. Recommendations for Businesses Targeting the EU Market

- Prepare for supply chain risk management early, especially SMEs.

- Strengthen systemic and proactive risk management rather than reactive measures.

- Use digital technologies and third-party risk data for independent supply chain assessments.

|

|

Source:Federal Ministry for Economic Cooperation and Developmen of SME Compass (2024), Complied by ITSI of ITIS (2024)